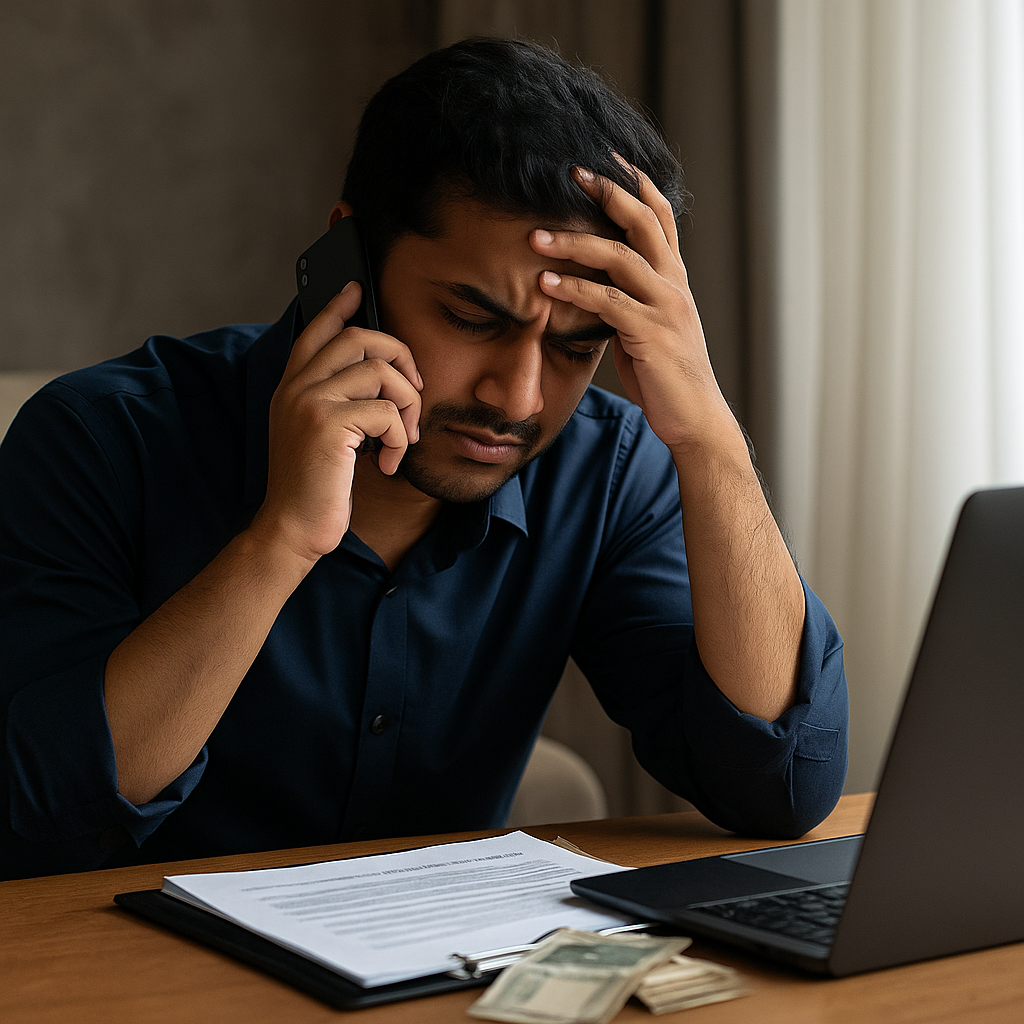

Loan recovery is a legitimate process — but harassment is not. In recent years, many borrowers have reported facing threatening calls, repeated messages, and even public shaming from recovery agents. While financial obligations must be honoured, no individual should be subjected to illegal or unethical recovery practices.

This article will help you understand what constitutes harassment, your legal rights, and the practical steps you can take to handle the situation — with Minpay, a financial wellness platform, supporting you through better money management and repayment strategies.

Knowing About Harassment of Recovery Loan Agents

Loan recovery agents are appointed by banks or lending institutions to collect overdue payments. However, some agents resort to aggressive or unlawful methods to pressure borrowers into paying, such as:

- Repeated calls at odd hours

- Use of abusive or threatening language

- Visiting your workplace or contacting relatives

- Publicly shaming you or revealing your debt to others

- Misrepresentation as government officials or legal authorities

Such tactics are strictly prohibited by the Reserve Bank of India (RBI) and other regulatory bodies globally. While lenders can pursue legal means to recover loans, harassment violates multiple consumer protection and privacy laws.

Key point: You have the right to be treated with respect and dignity, regardless of your financial situation.

Know Your Legal Rights

Understanding your legal protections is the first step in dealing with harassment. Here are some essential rights you should be aware of:

- Right to Privacy: Agents cannot disclose your debt details to third parties (friends, employers, or relatives) without consent.

- Right to Fair Treatment: The RBI and consumer protection laws prohibit harassment, intimidation, and verbal abuse.

- Permissible Contact Hours: As per RBI guidelines, agents can only contact borrowers between 7 a.m. and 7 p.m. in India (similar rules apply in other countries).

- Written Notices Only: Any legal notice must come from the bank or financial institution, not the agent personally.

- Complaint Channels: If harassment continues, you can lodge complaints with the lender, RBI Ombudsman, consumer courts, or local police.

Tip: Always keep a record of phone calls, messages, and visits by agents. This documentation strengthens your case if you need to take legal action.

Steps to Take if You’re Facing Harassment

If recovery agents cross the line, here’s a practical step-by-step plan to regain control:

- Stay Calm and Don’t Engage Emotionally

Avoid reacting in anger. Politely inform them that their behaviour is inappropriate and that you know your rights.

- Ask for Written Communication

Request that all future communication be made in writing. This creates a paper trail and discourages abusive calls.

- File a Complaint with the Lender

Inform the bank or NBFC about the harassment. Reputable institutions take such complaints seriously and may change the recovery agent.

- Approach the Ombudsman or Regulatory Authority

If the lender doesn’t act, escalate your complaint to the RBI Ombudsman or relevant authority in your country.

- Seek Legal Protection

You can file a complaint with the police under sections related to criminal intimidation, defamation, or trespassing.

- Explore Financial Solutions

Consider restructuring the loan, asking for a moratorium, or using platforms like loan settlement agency Delhi to create a sustainable repayment plan and avoid future defaults.

How Minpay Can Support Your Financial Wellness

Minpay is a trusted financial wellness platform that empowers individuals to manage debt smartly, avoid defaults, and regain financial stability. Here’s how Minpay can help you:

- ✅ Personalized Repayment Plans: Minpay assesses your income, expenses, and obligations to create a realistic and manageable loan repayment schedule.

- 📊 Budgeting & Expense Tracking: Gain visibility into your finances and identify areas where you can save or reallocate funds toward loan repayments.

- 🔔 Timely Reminders: Avoid missed EMIs with automated alerts, reducing the chances of recovery actions.

- 🛡️ Advisory & Legal Support: Minpay connects you with financial advisors and legal experts to handle harassment or negotiate with lenders.

- 🌐 Digital Dashboard: A simple, secure platform that helps you monitor all loans and repayment progress in one place.

By partnering with Minpay, you can take proactive steps to prevent harassment before it starts, through timely repayments and transparent communication with lenders.

Build Financial Resilience for the Future

While harassment by loan recovery agents can be traumatic, it’s also a wake-up call to reassess financial habits. Building financial resilience ensures that such situations don’t repeat. Here’s how:

- Emergency Fund: Save at least 3–6 months’ expenses for emergencies.

- Avoid Over-Borrowing: Borrow only what you can realistically repay.

- Prioritize High-Interest Debts: Clear high-interest loans (like credit cards) first to reduce overall burden.

- Automate Payments: Set up auto-debit or Minpay reminders to never miss due dates.

- Seek Professional Advice: If overwhelmed, financial advisors or platforms like Minpay can guide you through restructuring or consolidation options.

Financial wellness is not just about avoiding default — it’s about gaining control, building habits, and using the right tools to stay debt-free.

FAQs

1. Can recovery agents call me at night or early morning?

No. As per RBI guidelines, they can only contact you between 7 a.m. and 7 p.m. Any contact outside these hours is considered harassment.

2. What if the agent visits my workplace?

Agents are not allowed to shame or discuss your debt with colleagues publicly. You can file a complaint against such behaviour.

3. Can I be arrested for loan default?

Not a crime, loan default is a civil matter. You cannot be arrested for defaulting, but lenders can take civil legal action (like recovery suits).

4. What if the harassment continues despite complaints?

You can escalate to the RBI Ombudsman, file a police complaint, or approach consumer courts for compensation and protection.

5. How can Minpay help me avoid harassment?

By creating structured repayment plans, providing reminders, and offering advisory support, best loan settlement consultants in Delhi help you stay current on payments and handle lender communication professionally.

Final Thoughts

Loan recovery harassment is a serious violation of consumer rights. You don’t have to endure threats, public shaming, or intimidation. By knowing your rights, taking timely action, and using tools like Minpay to improve your financial health, you can resolve debts confidently and peacefully.